Adjustable vs Final Taxes in Pakistan: A Complete Guide to Withholding Taxes

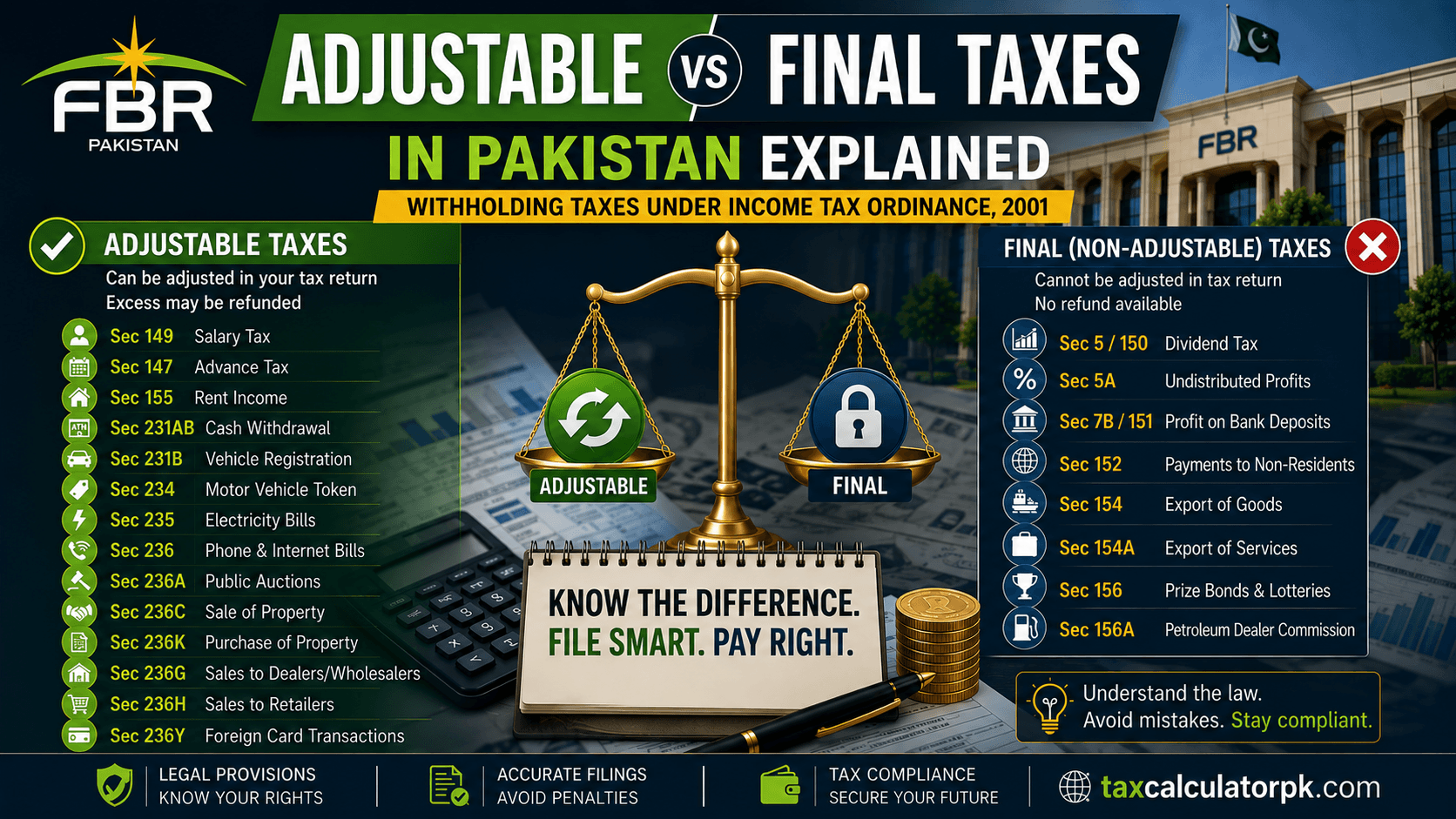

Pakistan’s Income Tax Ordinance, 2001 divides the withholding tax system into two major categories. This distinction helps determine whether a tax deducted during the year can later be adjusted or refunded, or whether it is treated as a final tax liability.

Understanding this difference is important because many taxpayers mistakenly assume that every tax deducted from their salary, utility bills, banking transactions, or property dealings can be claimed back. In reality, some taxes are adjustable, while others are considered final and cannot be refunded or adjusted through your annual income tax return.

What Are Adjustable Taxes?

Adjustable taxes are withholding taxes that can be adjusted against your annual income tax liability when filing your income tax return. If more tax has been deducted than your actual liability, you may even become eligible for a refund from the Federal Board of Revenue (FBR).

Below are some of the most common adjustable withholding taxes under Pakistan’s Income Tax Ordinance, 2001.

Salary Tax (Section 149)

If you are a salaried employee, your employer deducts income tax from your monthly salary under Section 149 and deposits it with the FBR on your behalf.

Advance Tax (Section 147)

Businesses and certain taxpayers pay advance income tax in quarterly installments under Section 147. These payments are later adjusted against the taxpayer’s final annual tax liability.

Rent Income (Section 155)

If you receive rental income, the tenant (or withholding agent) deducts tax under Section 155 before making payment. This tax is adjustable when filing your tax return.

Cash Withdrawal Tax (Section 231AB)

When a non-filer withdraws cash from a bank account beyond the prescribed limit, the bank deducts withholding tax under Section 231AB.

Vehicle Registration Tax (Section 231B)

Tax collected during the purchase or registration of a new motor vehicle is deducted under Section 231B by the relevant vehicle registration authority.

Motor Vehicle Token Tax (Section 234)

Annual token tax and vehicle fitness tax are collected under Section 234 by the provincial Excise Department.

Electricity Bills (Section 235)

Electricity distribution companies deduct withholding tax on electricity bills under Section 235.

Telephone and Internet Bills (Section 236)

Telecommunication companies deduct withholding tax on telephone and internet services under Section 236.

Public Auctions (Section 236A)

Tax on goods sold through public auctions is collected by the auctioneer under Section 236A.

Sale of Property (Section 236C)

Tax is collected under Section 236C when immovable property is sold. The relevant registration authority collects this withholding tax during the transfer process.

Purchase of Property (Section 236K)

Similarly, tax is collected under Section 236K when purchasing immovable property.

Sales to Distributors and Dealers (Section 236G)

Manufacturers and importers deduct withholding tax under Section 236G when selling goods to distributors, dealers, or wholesalers.

Sales to Retailers (Section 236H)

Sales made to retailers are subject to withholding tax under Section 236H.

Foreign Transactions Through Cards (Section 236Y)

Banks collect withholding tax under Section 236Y when customers make foreign transactions using ATM, debit, or credit cards.

What Are Final (Non-Adjustable) Taxes?

Final taxes, also called non-adjustable taxes, become the taxpayer’s final tax liability once deducted.

These taxes:

- Cannot be adjusted through the annual tax return.

- Cannot be claimed as a refund.

- Fully discharge the tax liability relating to that particular income.

Dividend Tax (Sections 5 & 150)

When a company distributes dividends to shareholders, it deducts tax under Sections 5 and 150 before making payment.

Tax on Undistributed Profits (Section 5A)

Companies may also become liable under Section 5A if profits are not distributed according to the applicable provisions of the law.

Profit on Bank Deposits (Sections 7B & 151)

Banks deduct final withholding tax on profit earned from savings accounts and deposits under Sections 7B and 151.

Payments to Non-Residents (Section 152)

Certain payments made to non-residents are subject to withholding tax under Section 152, which is deducted by the payer or withholding agent.

Export of Goods (Section 154)

Banks and authorized dealers deduct final tax on export proceeds of goods under Section 154.

Export of Services (Section 154A)

Exports of services are subject to final withholding tax under Section 154A.

Prize Bonds, Lotteries, and Winnings (Section 156)

Organizations distributing prizes, lottery winnings, or similar rewards deduct final tax under Section 156 before making payment.

Petroleum Dealer Commission (Section 156A)

Oil marketing companies deduct final withholding tax under Section 156A on commissions earned from the sale of petroleum products.

Key Difference Between Adjustable and Final Taxes

| Adjustable Taxes | Final Taxes |

|---|---|

| Can be adjusted in your income tax return | Cannot be adjusted |

| Excess tax may be refunded | No refund available |

| Reduces annual tax liability | Tax liability is considered fully discharged |

| Reported in the annual return for adjustment | Generally treated as the final tax on that income |

Pakistan’s withholding tax system covers a wide range of financial transactions, from salaries and property purchases to banking, exports, and dividends.

Knowing whether a particular withholding tax is adjustable or final helps taxpayers file accurate income tax returns, claim legitimate adjustments, and avoid losing money simply because they were unaware of the applicable tax rules.

Tags