Many people in Pakistan believe that agricultural income is completely tax-free. However, the actual legal position is more complicated.

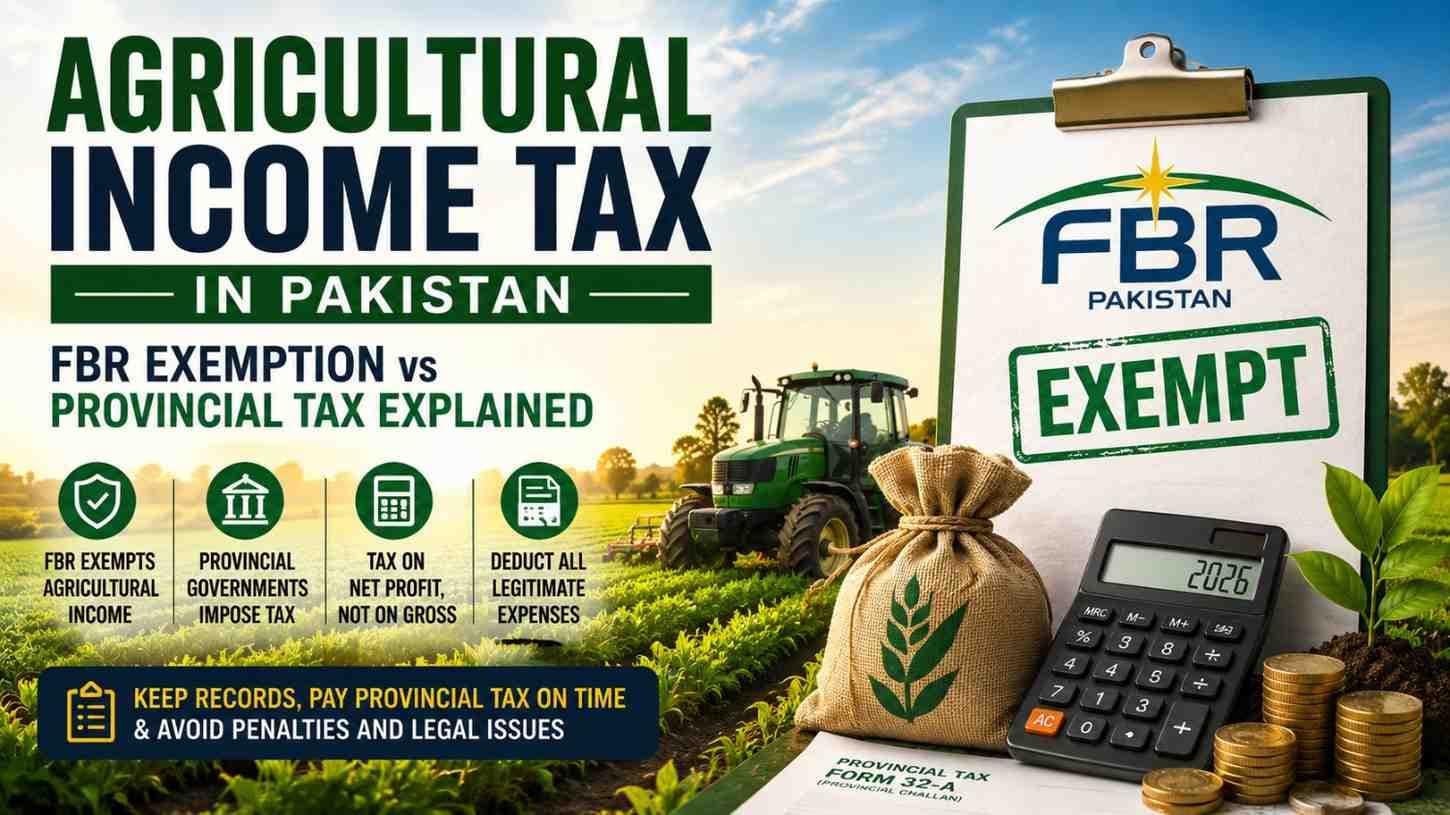

While the FBR does not impose federal income tax on agricultural income, that does not mean the income is entirely exempt from taxation.

If agricultural income is declared incorrectly or provincial tax obligations are ignored, taxpayers may later face notices, penalties, or legal complications.

Why FBR Does Not Tax Agricultural Income

Under Pakistan’s tax system, agricultural income is treated as exempt income for federal income tax purposes.

This means:

- Agricultural income is declared in the income tax return.

- But the FBR does not charge federal income tax on it.

When filing a tax return through the IRIS portal, agricultural income is usually reported under the “Exempt Income” section.

However, this exemption applies only to federal taxation.

Provincial Governments Can Still Tax Agricultural Income

The authority to tax agricultural income belongs to provincial governments, not the federal government.

For example:

- Punjab taxes agricultural income under Punjab laws.

- Sindh taxes it under Sindh laws,

- And the same applies in other provinces.

This is where many taxpayers become confused.

People often declare agricultural income in their FBR return, but later receive notices from:

- DC offices,

- Provincial revenue authorities, or

- Agricultural tax departments.

FBR Shares Agricultural Income Data

When filing a return on the IRIS portal, taxpayers usually provide:

- Province name,

- Tehsil details,

- Net agricultural income amount.

Although the FBR itself does not tax this income, the information may be shared with relevant provincial authorities.

As a result, provincial departments can later demand agricultural income tax based on the declared figures.

Agricultural Tax Applies to Net Profit, Not Gross Sales

One of the most important legal points is that agricultural tax is generally imposed on net agricultural profit, not on total sales or gross income.

This means taxpayers can deduct legitimate farming expenses before calculating taxable agricultural income.

Common deductible expenses may include:

- Seeds

- Fertilizer

- Spray and pesticides

- Labor expenses

- Harvesting costs

- Tube well electricity bills

- Machinery rent

- Lease payments (if land is leased)

After deducting these expenses, the remaining profit becomes taxable agricultural income.

Keep Proper Expense Records

Maintaining proper documentation is extremely important for anyone declaring agricultural income.

Taxpayers should preserve:

- Expense receipts

- Purchase invoices

- Lease agreements

- Utility bills

- Crop sale records

- Farming expense ledgers

If a provincial authority later issues a notice or inquiry, these records can help prove the legitimacy of deductions and declared income.

New Agricultural Tax Slabs for 2026

New agricultural tax slab rates for 2026 have already been implemented in Pakistan, and agricultural tax liability is calculated according to provincial slab structures.

The payment process is also provincial and is commonly completed through:

- Form 32-A (Provincial Challan)

Some taxpayers wait until they receive an official notice before paying agricultural tax. However, unnecessary delays may result in:

- Penalties,

- Surcharges,

- Additional notices, or

- Legal complications.

Final Thoughts

Agricultural income may be exempt from federal income tax under the FBR system, but it is still taxable under provincial laws.

That is why taxpayers should:

- Declare accurate net agricultural income,

- Maintain complete expense records, and

- Pay provincial agricultural taxes on time.

Proper compliance can help avoid future notices, penalties, and unnecessary legal problems.

Tags