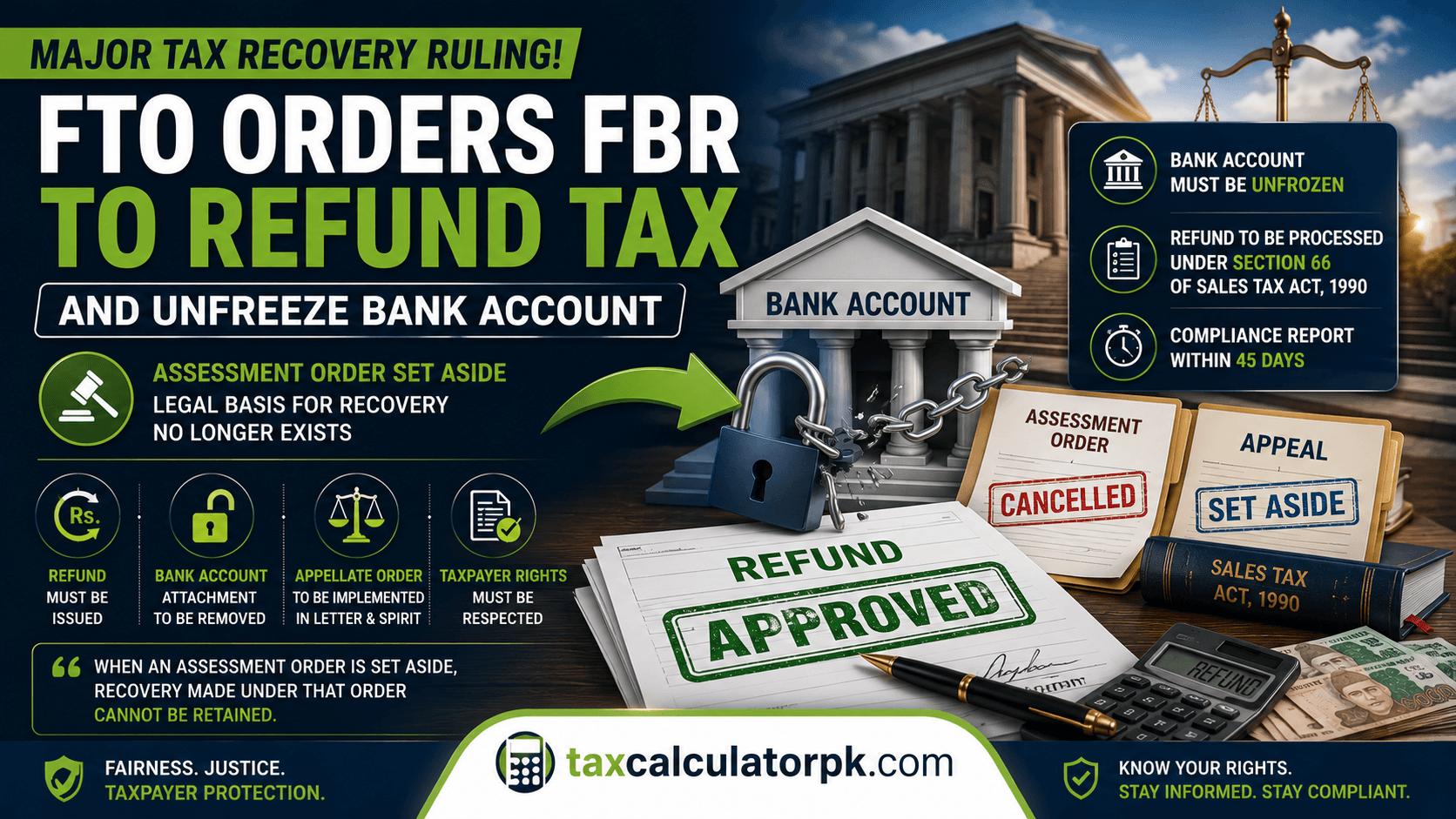

Major Tax Recovery Ruling: FTO Orders FBR to Refund Tax and Unfreeze Bank Account

In a significant ruling for taxpayers, Pakistan’s Federal Tax Ombudsman (FTO) has directed the Federal Board of Revenue (FBR) to immediately process a tax refund and remove the attachment placed on a taxpayer’s bank account.

The decision reinforces an important legal principle: once an assessment order is set aside on appeal, the legal basis for any tax recovery made under that order no longer exists.

Background of the Case

The case involved M/s Horizon Alloys (Pvt.) Ltd., against whom an ex-parte assessment order had been issued under Section 11E of the Sales Tax Act, 1990.

The company was accused of purchasing goods from a supplier that was later blacklisted by the FBR.

However, according to the facts presented in the case:

- The supplier was active in the FBR’s records at the time the purchases were made.

- The FBR subsequently restored the supplier’s active status.

- Despite these developments, the FBR recovered approximately PKR 24.5 million directly from the company’s bank account.

Assessment Order Was Set Aside on Appeal

The company challenged the assessment order before the Commissioner (Appeals).

The appellate authority set aside the assessment order and remanded the matter back to the tax authorities for re-adjudication.

Following this decision, the taxpayer argued that:

- The original assessment order no longer existed.

- The tax recovered under that order should be refunded immediately.

- The attachment on the company’s bank account should also be removed.

Despite these arguments, the FBR neither issued the refund nor released the bank account, leading the taxpayer to file a complaint before the Federal Tax Ombudsman.

FBR’s Position

The FBR argued that fresh proceedings were still pending and that, under the law, the reassessment process could continue until June 30, 2028.

Based on this, the department maintained that the recovered amount should not yet be refunded.

Federal Tax Ombudsman’s Decision

The Federal Tax Ombudsman rejected the FBR’s position.

According to the ruling, future or potential tax liabilities cannot justify withholding money that was recovered under an assessment order that no longer has legal effect.

The Ombudsman emphasized an important legal principle:

Once an appellate authority sets aside an assessment order, that order ceases to exist in the eyes of the law. Consequently, any recovery made solely on the basis of that order also loses its legal foundation.

The ruling clarified that while the FBR is free to conduct fresh proceedings and issue a new assessment if warranted, it cannot continue retaining money recovered under an invalid assessment order.

Refund Under Section 66 of the Sales Tax Act

The Ombudsman also highlighted Section 66 of the Sales Tax Act, 1990, which governs tax refunds.

According to the decision:

- If a valid refund application has been submitted,

- The tax department must process the application in accordance with the law,

- Any refundable amount should be released without unnecessary delay.

The ruling further clarified that issuing the refund does not prevent the FBR from completing the reassessment proceedings in the future or determining any tax liability that may lawfully arise.

Directions Issued to the FBR

The Federal Tax Ombudsman directed the FBR to:

- Immediately remove the attachment from the company’s bank account.

- Complete proceedings in accordance with the appellate order.

- Decide the refund application filed under Section 66 of the Sales Tax Act.

- Refund any amount legally found to be refundable.

- Submit a compliance report within 45 days.

Why This Decision Matters

This ruling strengthens an important protection for taxpayers in Pakistan.

It confirms that when an assessment order is set aside on appeal, the FBR cannot continue relying on that order to:

- Retain recovered tax amounts,

- Freeze or attach bank accounts, or

- Enforce recovery measures based solely on an invalid assessment.

While the FBR may initiate fresh proceedings where permitted by law, it must also respect taxpayers’ legal rights throughout the process.

The decision serves as an important reminder that tax authorities must act within the limits of the law and that appellate decisions have immediate legal consequences.