Have you ever wondered how the FBR discovers that someone’s wealth is greater than their declared income?

Hiding wealth may seem easy, but hiding its financial trail is much harder.

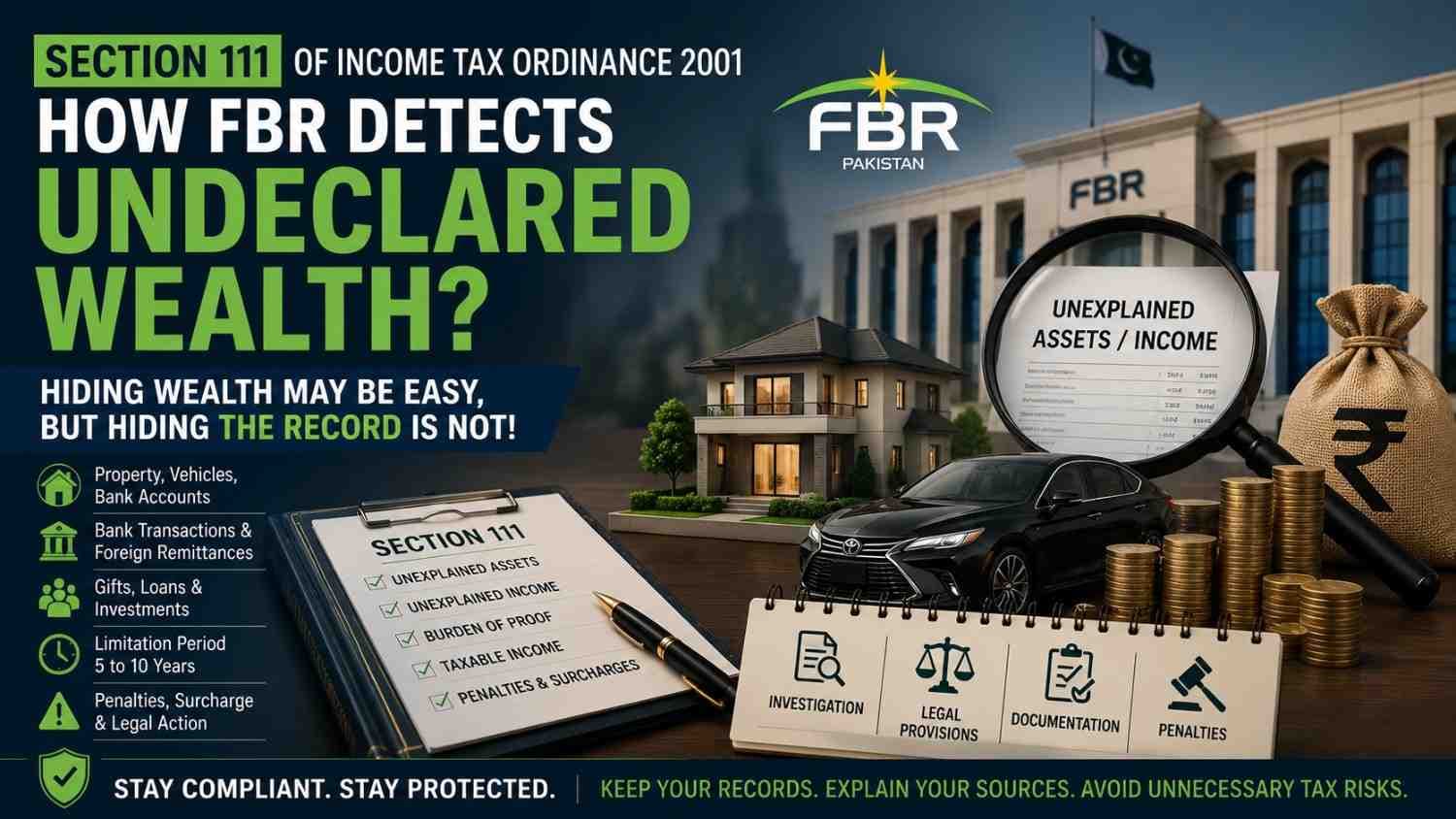

Section 111 of the Income Tax Ordinance 2001 is considered one of the most powerful and widely discussed provisions in Pakistan’s tax system. Commonly known as the law relating to “Unexplained Income or Assets,” this section allows the FBR to question taxpayers when their assets, expenses, investments, or banking transactions appear inconsistent with their declared income.

This is why Section 111 is frequently used in cases involving:

- Property purchases

- Expensive vehicles

- Large banking transactions

- Foreign remittances

- Business investments

- Lifestyle and unexplained expenditures

What Is the Purpose of Section 111?

The primary purpose of Section 111 is to ensure that every taxpayer can legally explain the source of their wealth and expenditures.

If a person possesses assets, investments, or funds without a clear documented source, the Commissioner Inland Revenue may treat those amounts as “unexplained” and classify them as taxable income.

In simple terms, the law asks one fundamental question:

“Where did this money come from?”

When Can FBR Invoke Section 111?

The FBR may initiate proceedings under Section 111 in several situations, including:

- Purchase of high-value property

- Ownership of luxury vehicles

- Large or unusual bank transactions

- Expenses exceeding declared income

- Investments inconsistent with reported earnings

- Assets significantly higher than known income sources

If the financial profile of a taxpayer does not match their declared income, the FBR may demand explanations and supporting evidence.

Burden of Proof Lies on the Taxpayer

One of the most important legal concepts in Section 111 is the “Burden of Proof.”

Initially, the responsibility lies with the taxpayer to prove the legitimate source of funds, assets, or investments.

Common supporting documents may include:

- Bank statements

- Sale agreements

- Gift deeds

- Inheritance documents

- Loan agreements

- Investment records

If sufficient evidence is provided, the FBR must legally examine and evaluate those documents fairly.

However, if the taxpayer fails to provide a satisfactory explanation, the unexplained amount may be added to taxable income.

Why Gifts, Loans, and Foreign Remittances Become Controversial

In Pakistan, many Section 111 disputes arise from:

- Gifts

- Loans

- Foreign remittances

In the past, taxpayers often relied on foreign remittances as a defense. However, Pakistani courts later clarified that merely receiving money through a banking channel is not enough.

The taxpayer must also establish:

- The real source of funds

- The identity of the actual sender

- The financial capacity of the sender

If a transaction appears artificial, undocumented, or lacks genuine financial substance, the FBR may reject the explanation.

Benami Transactions and Accommodation Entries

Another important legal issue connected with Section 111 involves:

- Benami assets

- Accommodation entries

- Paper transactions designed to whiten money

If assets are held in someone else’s name while the real owner is hidden, or if fake transactions are used to justify unexplained wealth, additional laws may also apply.

In major financial investigations, Section 111 is often linked with:

- Anti-money laundering laws

- Benami transaction laws

- Financial crime investigations

Final Thoughts

Section 111 gives the government significant authority to investigate unexplained wealth, suspicious investments, and undocumented income sources.

At the same time, Pakistani courts have consistently emphasized that these powers must be exercised fairly, legally, and based on proper evidence.

That is why Section 111 remains one of the most sensitive and impactful provisions within Pakistan’s tax system today.

Tags